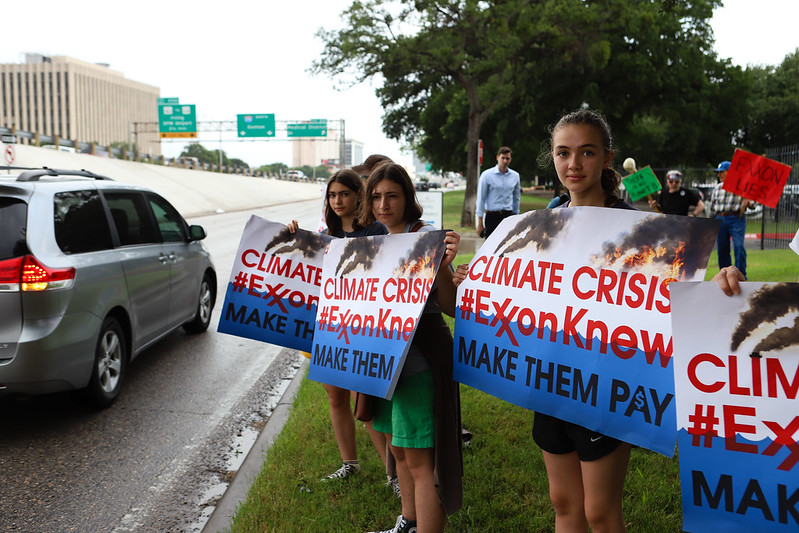

In recent years activist investors have pushed for, and won, sweeping changes to corporate policies, turning the shareholder proposal into a powerful form of dissent from within. The most frequently targeted corporations include Chevron and ExxonMobil, whose shareholders have pushed for action on climate change and other issues for decades.

But now, at a time when this type of shareholder activism has been rising for decades, the Trump administration has proposed new rules that would make it significantly harder for investors to challenge corporations at annual shareholder meetings.

Of the 400-plus shareholder proposals on the table this year, 21% involve climate change or other environmental issues. Another 18% seek changes in corporate political activity, while 11% concern human rights, according to analysis published in Proxy Preview 2020, an annual report tracking environmental, social and corporate governance proposals brought by shareholders.

Heidi Welsh, executive director of the Sustainable Investments Institute, a nonprofit that provides research to institutional investors, says activist shareholders appreciate the chance “to raise very touchy issues, get publicity through it, and talk directly to the board and other investors.”

Corporate boards, on the other hand, don’t tend to share the same appreciation. Companies aren’t as comfortable having explosive concerns aired in “the public eye…where they cannot necessarily control what is said about them,” says Welsh, whose organization produces the Proxy Preview with the nonprofit shareholder activist organization As You Sow and Proxy Impact, a shareholder advocacy and proxy voting service.

Despite corporate discomfort with the process, it often works in activists’ favor. Companies are known to adopt proposals that receive significant shareholder support, even if they fail to pass, or negotiate with proponents to address raised issues, in exchange for withdrawing the proposal from shareholder consideration. Successful shareholder proposals have ushered in Wall Street sea changes on a myriad of issues, including corporate sustainability reporting, and forced companies to detail their plans for reducing carbon emissions and develop plans and benchmarks to better manage water and other resources. The successes have occurred roughly at the same time as emerging technologies, such as satellite imagining exposing real-time deforestation and carbon accounting tools for tracing companies’ footprints though supply chains, that have made it harder for corporations to hide their true impact from the public and from shareholders.

The changes proposed by the U.S. Securities and Exchange Commission, due to be finalized this spring, are viewed as an attack on shareholder rights by many nonprofit organizations, interfaith groups, and other activist groups and institutional investors.

Petitions on political spending, as well as climate change and other environmental issues, are among those expected to decline the most under the new rules.

The SEC proposal acknowledges that the rules aim to shrink the number of shareholder proposals that pass the Commission’s review each year by an estimated 7%. The agency claims the changes are necessary modernizations to the shareholder petition process that will save corporations money by making it harder for frivolous proposals from so-called “gadfly” investors — small shareholders who some in the business community say force “nuisance” proposals onto corporate ballots.

But an analysis of proposals brought by individual investors suggests that other shareholders tend to support the issues raised by these gadflies. The investment research firm MSCI Inc. examined more than 2,300 shareholder proposals at U.S. companies from 2015 to 2019 and found that nearly a third of them were submitted by individual investors — not large institutions — and one-third won a majority of votes.

Silencing Dissent

Critics of the proposed rules say they will silence the voices of small investors while providing cover for a small number of large corporations. The authors of Proxy Preview and the report’s cosponsors — more than a dozen “green” and “sustainable” investor organizations, asset managers and private foundations — have denounced the moves as an unprecedented rights rollback.

They also note that these changes have been sought for years by a few big companies and trade associations like the Business Roundtable, the U.S. Chamber of Commerce and the National Association of Manufacturers.

“The SEC’s role is to be the investor’s advocate, protecting investor interests. The message from these comments is clear that the SEC should put aside these two proposals that reflect a disturbing anti-investor bias,” Tim Smith of Boston Trust Walden said in a statement put out with other commentary from members of the Shareholder Rights Group, which oppose the new rules.

The proposed changes “represent the biggest attack on shareholder rights by the SEC since it was created in 1934,” wrote Ken Bertsch, executive director of the Council of Institutional Investors, in Proxy Preview.

Sanford Lewis, an attorney and director of the Shareholder Rights Group, calls the new rules “an opportunistic effort to roll back investor rights” that takes advantage of the Trump administration’s pro-business stance at a time when shareholder support for environmental and social proposals continues to grow.

Welsh, in a phone interview, echoed those sentiments, calling the rules “a power play” by forces that have wanted to “clamp down on the shareholder proposal process for a long time.”

What Would Change

Specifically, the proposed changes to Rule 14a-8 of the 1934 Securities and Exchange Act would reduce the number of investors who can bring a proposal.

Today, in order to get a proposal on a ballot, investors must own a minimum of $2,000 worth of stock. Under the new rules, ownership thresholds would range up to $25,000, adding new financial obstacles so-called “retail investors,” small investor who represent about 30% of stock ownership.

The change would also affect nonprofit groups that have, in recent decades, turned proxy season into protest season and annual shareholders’ meetings into platforms for directly confronting corporate executives. Groups can draw publicity to their causes through protests inside and outside of the annual meetings where the votes occur. For instance, dozens of activist organizations converged on Chevron’s annual meeting last May to confront CEO Michael Wirth over the company’s environmental and human-rights record.

“This is the one time that the Chevron CEO, board, and senior management are forced to listen to us. There were more climate & human rights speakers than at any shareholder meeting I’ve been to. We dominated the event & we made sure our voices were heard.” https://t.co/5KUc7Lti2P pic.twitter.com/cQPRk8g3To

— Paul Paz y Miño (@paulpaz) May 31, 2019

The SEC has also proposed complicated new requirements governing the percentage of votes a proposal must receive one year to qualify for resubmission if it doesn’t pass. If proposals don’t meet the higher new resubmission tests, investors would be barred from bringing the issue again for three years. This would knock out even proposals that receive significant support, which concerns investor groups because support for issues commonly rises and falls from one year to the next, as investors become more familiar with them. Most corporations already require a supermajority for passage of shareholder proposals, so successful proposals often take years to build support among stockholders.

Advocates say the new rule is particularly troubling in the case of climate change proposals, considering that, according to climate scientists, the world has less than a decade left to bring down climate-changing emissions and head off the worst impacts of climate change.

Lewis says a proposal to Chevron this year are among those that would be blocked from resubmission under the new rules.

He adds that he’s also concerned about the Trump administration’s new interpretations of climate change resolutions at several companies. For decades, activist investors have been asking corporations to detail plans to address climate change, making it what observers call “a proxy season classic.” But Trump’s SEC has allowed companies to block several proposals by reinterpreting them as efforts to micromanage “ordinary business,” a commonly used SEC exclusion provision.

The final new stumbling block comes from what’s been called a “companion” rule change, where the SEC is preparing a clampdown on proxy advisory firms that large institutional investors rely on for research and recommendations on the issues raised each season.

The Public Ignored

The SEC formally proposed the new rules last November after a 3-2 vote along party lines. That prompted substantial outrage in the activist investor community — along with a deluge of more than 14,000 angry comments from individual investors, faith-based groups, asset and pension fund managers, unions, and local government officials.

Despite that uproar, the SEC is expected to issue the new rules pretty much as proposed.

While the COVID-19 outbreak may slow the process, most observers expect the SEC to issue the final rules this spring to beat a deadline established by the Congressional Review Act, which would make the rules harder to repeal even if President Trump loses reelection in the fall. Investor groups are already preparing for legal challenges in a saga that may ultimately be determined by who wins the presidential election.

The SEC has acknowledged that the new rules will reduce the number of proposals that go to a vote each year. But several independent analyses forecast even bigger reductions in submitted proposals, particularly on issues related to climate change and “corporate political influence spending” on elections and lobbying.

Welsh’s institute told the SEC in a letter that the government’s analysis “substantially understates” how many proposals would fail the new resubmission tests, among other things.

“Three times as many proposals that went to votes over the course of the last decade on these issues would have been ineligible had the proposed rule been in place,” Welsh wrote.

Welsh says the rule changes would remove a valuable resource for boards of directors: the input of people outside the company.

“You can argue from a straight-up business perspective that it doesn’t make sense to eliminate a feedback loop that provides information for meaningful consideration,” Welsh says, noting that in the investment world more information “is generally seen as a good thing, not a bad thing.”

New York City Comptroller Scott M. Stringer and others who represent large institutional holders have made similar comments. Stringer said in a statement that the proposals “will only serve to insulate management and directors from accountability to shareholders.”

Groups from all over the US converged on the @usbank shareholders meeting at the @Albuquerque Hyatt @StopETP protest to demand that USB stop funding pipelines. #StopETP @CVNMActionFund @EnvNM @NewEnergyNM @WeAreOneRiver @RioGrandeSierra pic.twitter.com/uGE5xzCffE

— 350NM (@350NM) April 17, 2018

While all of this is going on, many corporations — already apparently emboldened by the pro-business Trump administration — show early indications that they will use the COVID-19 lockdowns to further diminish shareholder activism during this spring’s proxy season. In mid-April AT&T notified shareholder proponents that they would not be allowed to present their three proposals at the online shareholders’ meeting on April 24. Instead, the company instructed proponents to submit written statements that corporate management would read aloud. “Companies are trying to take advantage of COVID-19 and silence voices,” investor activist John Chevedden told Reuters.

A Boon to Big Business

MSCI’s analysis found the rules changes would primarily benefit about a dozen companies, each of which received four or more shareholder proposals a year — among them, oil companies Exxon Mobil Corp. and Chevron Corp.

Indeed, Welsh says, a close reading of the complicated resubmission formula indicates that the biggest impact will be on proposals on political activity such as corporate election spending and lobbying at very large companies like Exxon.

“It’s a very complicated resubmission rule that affects about nine proposals. I do think that’s telling,” she says. “This rule is written to restrict political influence spending proposals.”

Nevertheless, advocates say shareholder activism has become a force for good in society — and this year could be a pivotal one for people and the planet, said Andrew Behar, CEO of As You Sow. As he said in his remarks at the March launch of this year’s Proxy Preview, today’s growing demands for meaningful corporate climate action make shareholder activism in 2020 a year of “great risk but also one of great hope.”

“This year,” he said, “can be an inflection point, when the battle for the future of our planet truly intensifies and a new trajectory is revealed.”

![]()